I hope you enjoy reading this blog post. If you want to book a free consultation, click here.

Pregnancy is a period of profound transition for a woman and even the man. Between finding the right cradle for the baby and tracking its developmental milestones, expecting mother something starts thinking about that one thing she always put on hold — Term Insurance. But a question arises after that thought: Can a pregnant woman apply for term insurance in India?

The short answer is — yes. However, securing a term plan while expecting requires going through a certain set of underwriting rules. Because pregnancy introduces temporary physiological vulnerability, insurance companies approach these applications with ‘cautious neutrality’ i.e. they aren’t partial, but they take certain precautions. They adjust their decision based on the expectant’s trimester and medical metrics.

Term Insurance vs. Health Insurance: Clearing the Confusion

Before diving into the application process, it is vital to distinguish between two completely different financial tools:

- Maternity Health Insurance: This covers immediate, short-term hospital expenses, prenatal check-ups, and delivery costs (Normal or C-section). In India, you generally cannot buy maternity health insurance if you are already pregnant, as insurers treat it as a pre-existing condition requiring a mandatory 2-to-4-year waiting period.

- Term Life Insurance: This is pure life cover. It does not pay for your hospital stay or delivery bills. Instead, it ensures that if the worst should happen, your family and newborn receive a significant tax-free lump sum to replace lost income, settle debts and secure the child’s future needs such as education.

Unlike health insurance, term insurance plans have no maternity-related exclusions. If a policy is active, it covers death from any cause, including childbirth complications, starting from Day 1.

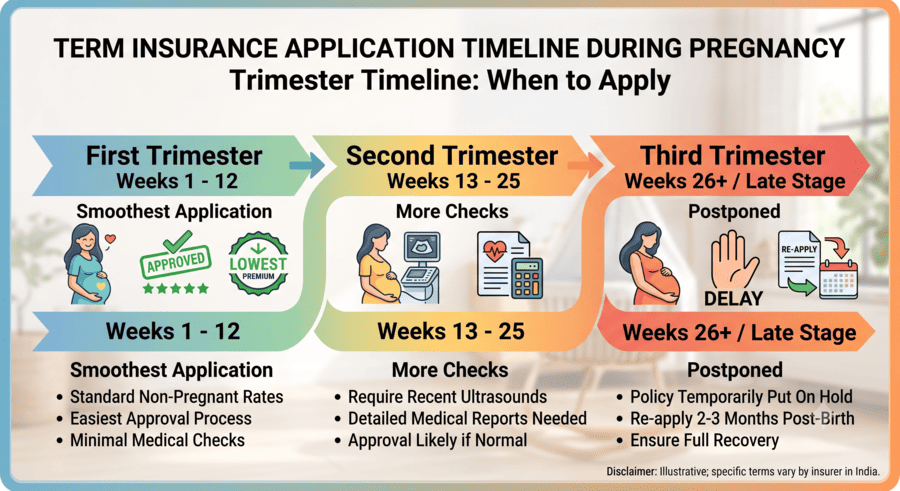

The Trimester Timeline: When to Apply

Your application timeline plays the biggest role in determining whether an insurer accepts, delays or adjusts your premium.

First Trimester (Weeks 1 to 12) – The Easiest Window

This is the ideal time to apply. Because your body has not yet undergone major metabolic shifts, and pregnancy-specific complications have rarely manifested, most insurers process applications smoothly at standard, non-pregnant premium rates.

Second Trimester (Weeks 13 to 25) – Still Workable

Approvals are still highly accessible during these weeks, but the underwriting department will pay closer attention. Expecting mothers will need to provide up-to-date ultrasound (USG) scans and routine blood reports to prove the pregnancy is progressing normally.

Third Trimester (Weeks 26 to Delivery) – The Defensive Zone

In late-stage pregnancy, insurers shift to a conservative approach. Due to the baseline, unpredictable risks associated with active childbirth, most Indian insurers will activate a Postponement Clause. This is not a rejection; the insurer simply places the file on hold and asks the mother to re-apply 60 to 90 days after a safe delivery.

What Happens Under the Hood? The Underwriting Hurdles

When you apply while pregnant, the insurance company will look closely at several components of your health:

Compulsory Gynaecological Records:

The applicant cannot simply fill out a basic health form. The insurance company will require her to submit:

- Every single ultrasound (USG) report conducted up to that date.

- Official antenatal care (ANC) booklets or consultation notes from the gynaecologist.

- If the doctor has noted a ‘High-Risk Pregnancy’ due to factors like placenta previa, multiple pregnancies (twins/triplets) or previous history of miscarriages/C-sections, the application process will immediately face friction.

Targeted Medical Screening:

Even if a woman feels perfectly healthy, the insurer will mandate a series of comprehensive medical tests to rule out any underlying risks. During pregnancy, these tests focus heavily on metabolic and cardiovascular spikes:

- Blood Sugar Tests (HbA1c / Glucose Tolerance): Insurers look specifically for Gestational Diabetes Mellitus (GDM). If a woman’s blood sugar spikes only during pregnancy, the insurer will likely postpone the policy until after childbirth to see if the levels return to normal.

- Blood Pressure Check: Underwriters closely monitor this to rule out Gestational Hypertension or Preeclampsia (a severe pregnancy complication characterized by high blood pressure), which is viewed as a high-risk condition. Urine Analysis: This is conducted to check for proteinuria (high protein levels in the urine, a sign of kidney stress or preeclampsia) and urinary tract infections.

- Complete Blood Count (CBC): Checked to rule out severe pregnancy-induced anemia (low hemoglobin levels), which can sometimes complicate delivery.

Insurers look specifically for temporary metabolic spikes, including Gestational Diabetes Mellitus (GDM) via HbA1c/glucose tests, and Gestational Hypertension (pregnancy-induced high blood pressure).

The “Postponement” Clause

The most common hurdle a pregnant woman faces—especially if she applies in her late second or third trimester (after week 24–26)—is a formal postponement.

What it means: The insurer does not reject the application. Instead, they officially state: “We are putting your application on hold. Please re-apply 60 to 90 days after a successful delivery.”

They do this because the physical stress of late-stage delivery introduces unpredictable variables that cannot be calculated by standard actuarial models.

Premium Loading & Limits

If you are in your first trimester but present mild risk factors like minor thyroid fluctuations or an elevated pre-pregnancy Body Mass Index (BMI), the insurer may approve the policy but apply a “loading fee”—permanently increasing your premium. Furthermore, if you are a homemaker, the maximum sum assured may be capped relative to your spouse’s income.

⚠️ The Golden Rule of Insurance: Always disclose the pregnancy on your proposal form, even if you are only a few weeks along. Hiding a pregnancy constitutes a non-disclosure of material facts, which gives the insurer the legal right to reject a family’s claim in the future. (Note: If you conceive after your policy is already active, you do not need to inform the insurer; your rates and coverage remain locked).

Lower Sum Assured Limits

If an expecting mother is a homemaker or doesn’t have an independent source of income, Indian insurers already cap the maximum life cover she can get based on her husband’s income. When pregnancy is added to the mix, insurers may further restrict the maximum sum assured they are willing to offer until the delivery is safely completed.

Building the Perfect Safety Net: Essential Riders for Mothers

Women in India already benefit from 15% to 20% lower term insurance premiums compared to men due to a higher statistical life expectancy. New mothers can maximize this affordability by adding critical, living-benefit riders to their base plan:

| Rider Name | What It Covers | Why New Mothers Need It |

|---|---|---|

| Critical Illness Rider | Provides a lump-sum payout upon diagnosis of a major condition (e.g., breast, ovarian, or cervical cancer). | Unlike health insurance, this money is paid directly to you. It handles experimental care, hiring domestic help, or keeping the household running during recovery. |

| Waiver of Premium (WOP) | Waives all future premiums if the mother suffers a permanent disability or critical illness. | Ensures the life insurance cover stays 100% active for the child, even if the mother loses her earning capacity due to a medical crisis. |

| Accidental Permanent Disability | Offers a lump-sum payout if an accident results in life-altering physical trauma. | Acts as a financial cushion to manage long-term rehabilitation or structural modifications to the home without draining family savings. |

Innovative Features to Look For

Several leading insurers in India have modern, women-centric features built into their term plans. For example, some policies offer a Premium Break during Pregnancy, allowing you to safely pause premium payments for up to 12 months during your maternity leave, ensuring your coverage doesn’t lapse when cash flows temporarily change.

The Takeaway

If you are planning to secure your family’s future, the best strategy is to apply during the first trimester to secure low, standard premium rates. If you have already crossed into the late second or third trimester, focus on a healthy delivery, gather your medical clear-bills and plan to apply three months after your baby arrives.

Share This Story, Choose Your Platform!

About the Author: Donald Gonsalves